ACH, or Automated Clearing House, is an electronic payment system that moves money between banks. Also known as an electronic check payment (or eCheck payment), ACH has been around for over 50 years and is considered a traditional way to pay electronically.

If ACH sounds familiar, it’s because it’s the technology that enables employees to receive their paychecks through direct deposit or for consumers to pay a bill online.

While the technology behind ACH has been around for decades, that doesn’t mean its usage is declining. Statistics around ACH in the 21st century are astounding. According to Nacha, the ACH network administrator, there were 6.8 billion ACH payments processed in Q3 of 2020, which is 9% higher than Q3 of 2019.

Additionally, the network continues to modernize itself by updating its rules to complement the payments industry’s current demands. Updates include the ability to transfer larger amounts of money in a shorter period, with the eventual goal of offering transactions that allow funds to settle and be available on the same day.

Today’s ACH options continue to benefit large enterprises and small businesses alike. Based on these growth numbers and technological advances, software developers should keep ACH functionality on their radar and consider its viability for their customers.

Understanding ACH Payment Processing

Where does ACH fit in the digital payments space? To fully appreciate how far ACH has come and its modernization efforts, it makes sense to look back at how it started.

The History of ACH

In the late 1960s, the proliferation of paper checks made California bankers take a step back. They were concerned that the current technology and equipment would not be enough to sustain future volumes. In response, they created SCOPE, which stood for “Special Committee on Paperless Entries.”

Simultaneously, the American Bankers Association conducted a study that looked for ways to improve the US’s payment system. These events led to the creation of the first ACH association that managed electronic payments. Following California’s lead, more regional ACH associations came into existence, and in 1974, the National Automated Clearing House Association, or Nacha, was formed to be an administrator to these associations.

The Evolution of ACH

US government entities such as the US Air Force and the Social Security Administration initially used ACH. Today, it’s how 93% of Americans get paid.

In 2001, making ACH payments online and over the phone became an option. It allowed consumers to pay monthly recurring items such as utility bills or conduct online transactions for other goods and services without writing and mailing a paper check.

ACH Modernization Efforts

Standard ACH transactions typically take 3-5 business days to initiate and settle. Part of the reason for this relatively longer timeline is that they process these transactions in batches submitted once a day at a specified time.

However, in 2016, Nacha began their rollout of Same Day ACH. To speed up the processing timeline, Nacha added two additional settlement windows that allowed banks to send batches either in the morning or the early afternoon, with settlement occurring by the end of the business day.

Note that Same Day ACH transactions have not replaced standard ACH transactions entirely. Instead, it is one option that bank originators can choose. Currently, same-day ACH comes with a separate transaction fee covering the costs of having two additional settlement windows available. Bank originators that do not opt-in will experience the longer settlement times associated with standard ACH transactions.

In March 2020, the maximum amount allowed for an ACH transfer increased tremendously from $25,000 to $100,000, spurring healthy growth in the number of payments and volumes processed in the latter part of 2020. A combination of modernization efforts, flexibility in settlements, and disruption of business practices from the pandemic may have kept the ACH network a valuable part of the payments ecosystem.

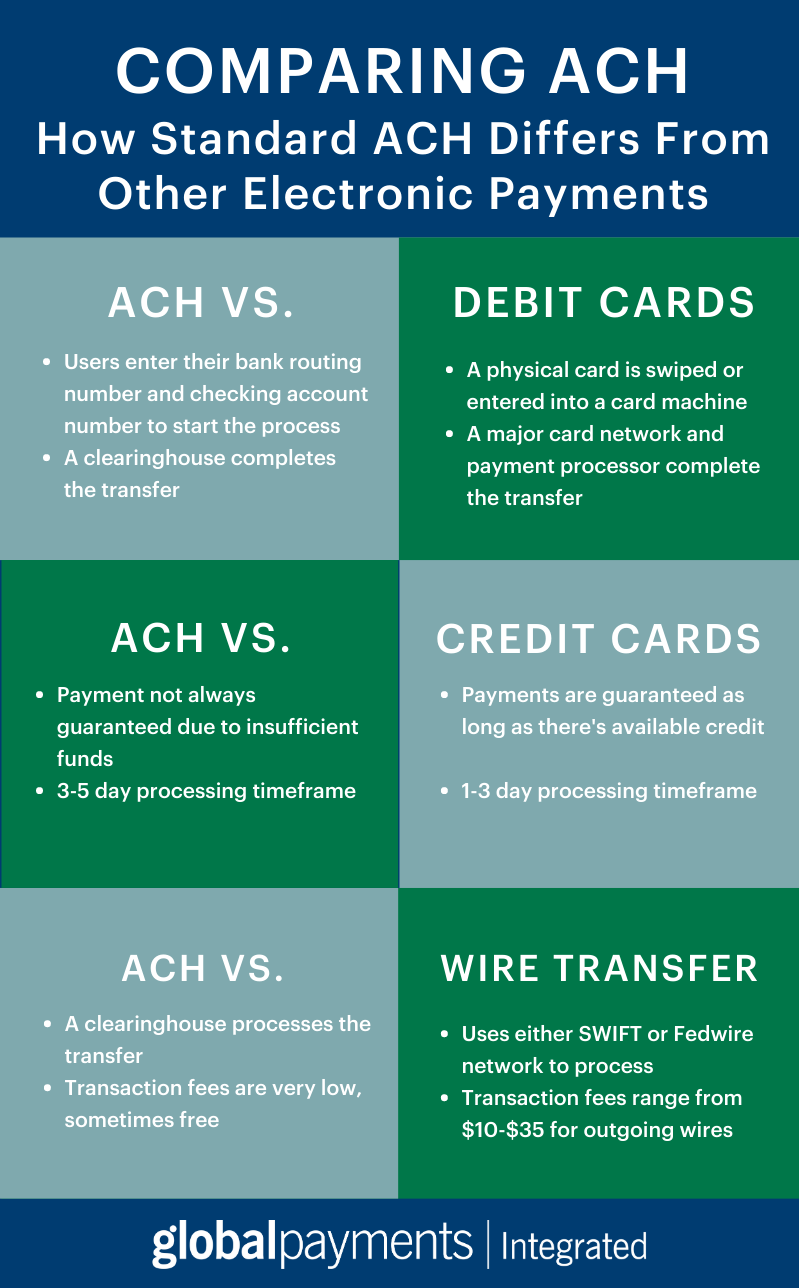

Comparing ACH to Other Electronic Payments

Here’s how standard ACH differs from other electronic payment methods.

ACH vs. Debit Cards

Since both transactions technically happen by withdrawing funds directly from a checking or savings account, it’s understandable to think that these two transactions are the same.

However, the difference lies in how they are processed. A major card network and a payment processor are needed to complete a debit card transaction, while a clearing house is required to connect the two banks involved in an ACH transaction.

Additionally, ACH and debit card transactions are accessed differently. To initiate an ACH, a user may need to log in to an online banking platform or submit a bank routing number and bank account number for the transaction. A debit card transaction may require a physical card and possibly a PIN or signature for authorization.

ACH vs. Credit Cards

Like debit cards, credit card transactions require a major card network and payment processor.

One significant difference is the “guarantee of payment.” As long as there are funds available in a user’s credit line, the card network will authorize the transaction in seconds and funds transfer within 24 hours at the earliest. Requesting ACH payments run the risk of withdrawing from accounts with insufficient funds or that are closed, making cash flow slightly unpredictable.

Processing times also differ; as mentioned above, if a bank originator is not using same-day ACH, you can expect a 3-5 day processing time frame. Credit cards average faster processing times, between 1-3 business days.

ACH vs. Wire Transfer

Similar to the concept of ACH, wire transfers electronically move funds from one financial institution to another. Their key differences lie in how they are processed and costs per transfer.

Banks process wire transfers themselves. Instead of the clearing house, they use a different network (such as SWIFT or Fedwire) to transfer money. The funds are received and usually accessible on the same day, making it the preferred way to send money for significant transactions such as a down payment for a home.

Because of their “one-off” immediate nature and the need for bank employees to occasionally review these transfers, wires are more expensive than ACH transfers. Banks can charge anywhere between $10-$35 for an outgoing wire transfer and a $10-$20 fee to the recipient for receiving the transfer. In contrast, many ACH transfers are free for consumers, and ACH for businesses charge much lower transaction fees.

Business Benefits for Accepting ACH

While ACH may not be as flashy as digital wallets or cutting edge like cryptocurrencies, it’s still a suitable payment option that growing businesses should implement.

It is worth noting that approximately 25% of US households do not have a credit card, and many B2B businesses still rely on checks for payments. These statistics suggest that companies could lose sales by not accepting eCheck payments.

Businesses that receive recurring revenues by selling subscriptions, memberships, or other living necessities charged monthly are good candidates for ACH processing. They can take advantage of ACH’s cost-effectiveness due to its low processing fees.

eChecks are another paperless payment option with a faster processing window than paper checks. Mailing paper checks add to the processing time. Additionally, employees will have to make an effort to go to the bank to get the checks deposited. These factors cause delays in payment that businesses can mostly avoid with eChecks.

eCheck payments are also more secure, as paper checks expose checking or savings account numbers each time. They can also be stolen or forged. With eChecks, the user only has to reveal their bank information once. If they choose to make recurring payments, they can set it and forget it. In turn, businesses will automatically receive funds on-time and have reliable cash flow.

Accepting ACH Transactions and eCheck Payments

Software developers can partner with a payment processor like Global Payments Integrated to include ACH transactions and eChecks as a payment option within their software. Our teams can ensure online payment forms are secure by tokenizing sensitive payment details, giving merchants peace of mind that they are actively safeguarding sensitive payment data. Contact us today for more details!

Michelle Mondonedo

Brand Marketing Manager